.jpg)

Preface

The below article was first published to HFI Research on Nov. 19 in our weekly flagship report. This was before the news media came out with leaks that OPEC is considering extending the production cuts to end of 2018. We explain below why we believe OPEC will announce the so-called "production cuts."

What should you expect from OPEC's upcoming meeting?

Verdict: OPEC will announce a deal extension to the end of 2018 on Nov. 30.

Abbreviated Reason: Long-term supply deficit is coming. OPEC, with its vast amounts of data, understands the implications of how much U.S. shale can grow. Our rigorous analysis of U.S. shale leads us to believe we will see ~700k b/d of growth next year compared to 1.4 to 1.6 million b/d of demand growth again in 2018. In addition, if OPEC announced the extension through the end of 2018 at the end of November, the steep backwardation in the oil curve will put further pressure on U.S. shale's servicing cost base.

The lower than prompt future prices also eliminate shale's ability to try and ramp production into a higher oil price environment, all the while OPEC benefits from higher prompt prices. Saudi Aramco's IPO at the end of 2018 also gives incentives for Saudi to push higher investor sentiment today. It needs all the time in the world to flip sentiment.

Explanation

We will break down this article into separate puzzle pieces. The puzzle pieces will lead from one to the other, so be sure not to skip around. We will explain to you the fundamental elements of why if OPEC makes a production cut extension announcement at the end of November nothing changes, and why it's better to announce sooner than later.

Puzzle Piece No. 1: Why did Saudi not cut oil production in 2014?

To understand the motivation of the Saudis, we first need to understand why it didn't cut oil production in 2014. In our article titled "Understanding History: Why Didn't Saudi Arabia Cut Oil Production In 2014?" we explained that at the time of the 2014 November OPEC meeting, forecasters from IEA, EIA, and OPEC noted that the growth in U.S. shale - which, at the time, was on pace for 1.2 million b/d year-over-year growth -would push the global oil market balances into oversupply. But what the consensus didn't forecast at the time was for oil prices to fall below $90/bbl. Here is an excerpt from the article:

None of these forecasts envisaged oversupply and a price collapse; all assumed stable prices through the end of the decade. Thus IEA, OPEC, and BP - and most market participants and industry - assumed OPEC would cut to keep prices stable.

The assumption baked into everyone's model at the time was that Saudi Arabia would want to keep production low in order to keep stability in the market. But what in turn happened was a massive disappointment.

For one, we agree that Saudi Arabia should not have cut production in 2014. Oil demand at that time was slowing as the China fiscal rebalancing took its toll on the broader economy. Europe was still recovering following the Greece crisis and had to contend with debt issues in Italy and Spain. The U.S. was the only beacon of light in the global economy. Demand grew YoY at that point in time less than 1 million b/d, and the Saudis bit the bitter pill and let the market free fall.

Now, why is understanding puzzle piece No. 1 so important? Because this gives you context as to what the Saudis are using to guide their decision-making process.

Puzzle Piece No. 2: It's all about the long term.

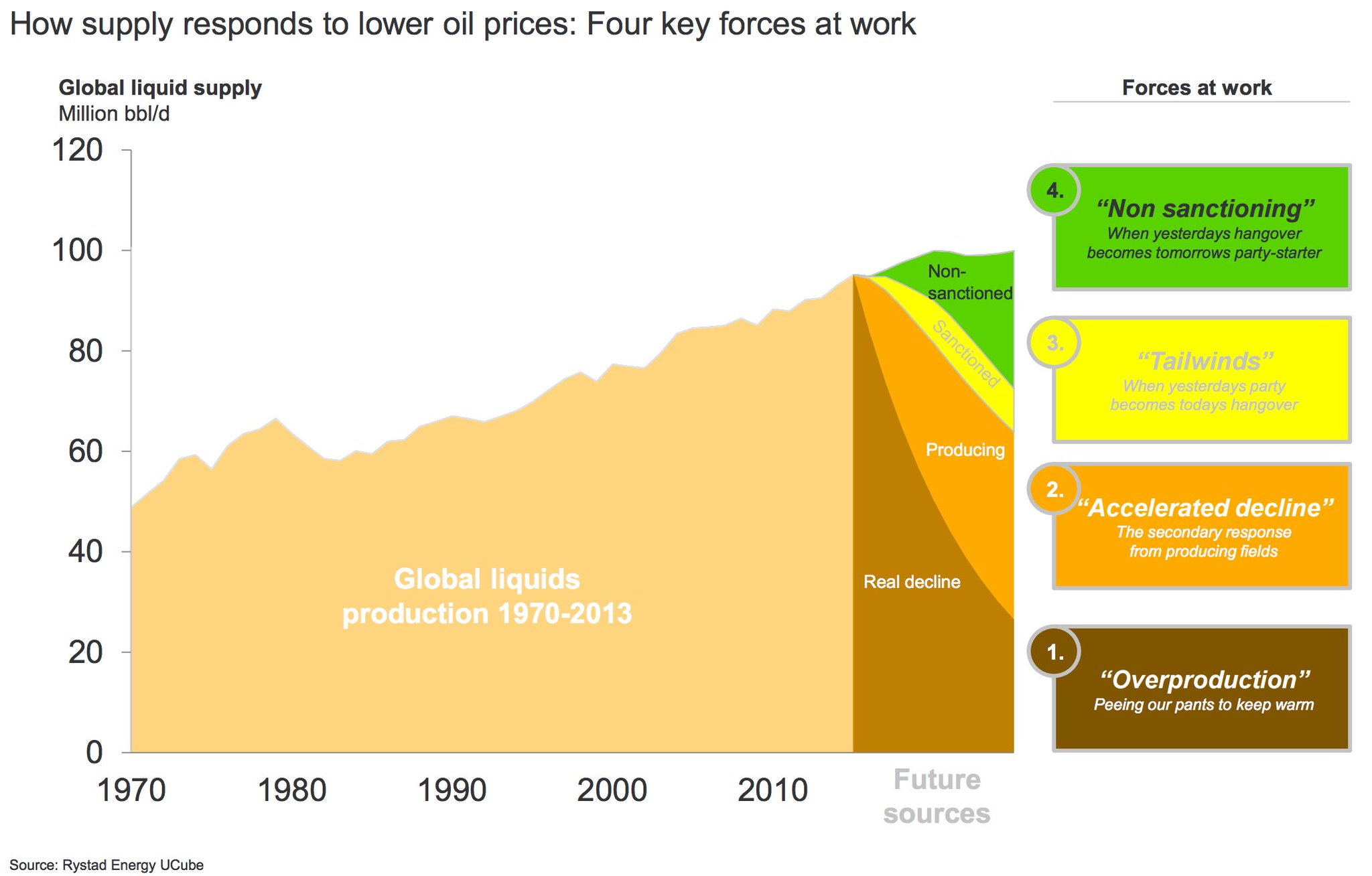

Our main bull oil thesis is that a supply deficit is coming, as illustrated by this simple chart from Rystad Energy:

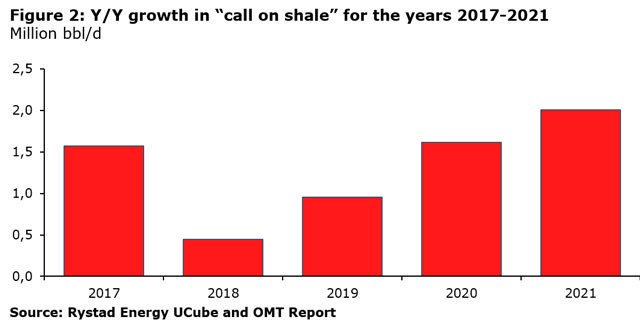

In addition, third party consultants like Rystad have already given Saudi the amount of supplies needed by shale:

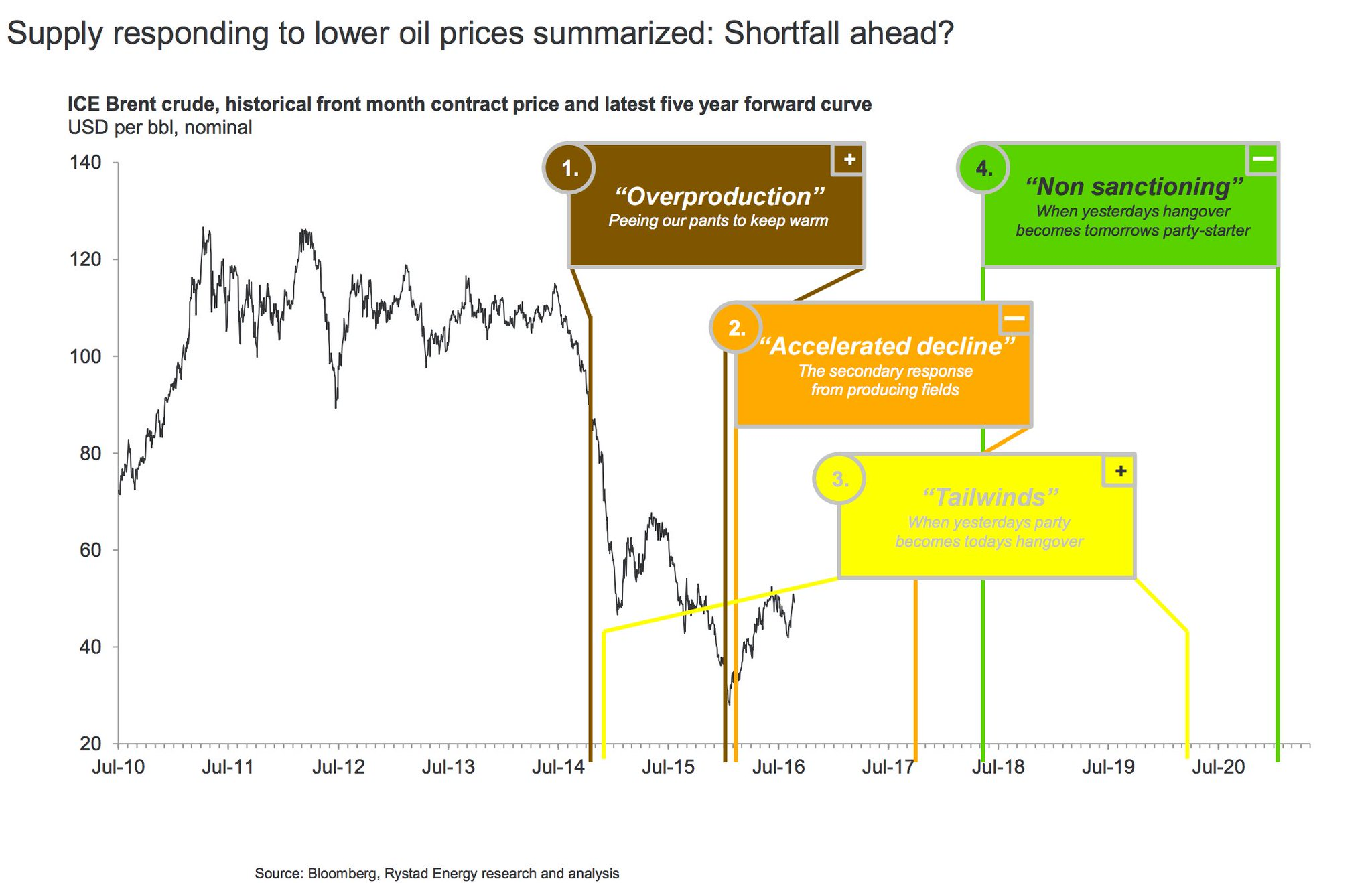

All of this leads to the following scenario:

Basically, what these charts show is that the world needs U.S. shale in the long term. Over the course of the last two years, U.S. shale has been flat, while demand has risen by more than 5 million b/d. This, alongside declines starting in Mexico, China, Colombia, and other non-OPEC states, will provide even stronger tailwinds ahead.

For Saudi, the same scenario that pushed them not to cut production in 2014 is now in complete reverse. The world is going to see a shortage in supplies, and there are no producers outside of OPEC and the U.S. that can provide the supplies needed in the years ahead.

So, the real question is: would the long-term oil fundamentals change if OPEC delayed the announcement of a production cut extension to the end of 2018? The answer is no.

Puzzle Piece No. 3: Capped capacity growth in U.S. shale.

For as much as we have written on the topic of U.S. shale, the consensus still appears benevolent to the facts. For one, commentators continue to point to rig count as an indication of U.S. shale growth, when it's well completions that matter. If we know that well completions are currently bottle-necked due to a lack of workers, then it's easy to see where max capacity of U.S. shale growth is in 2018.

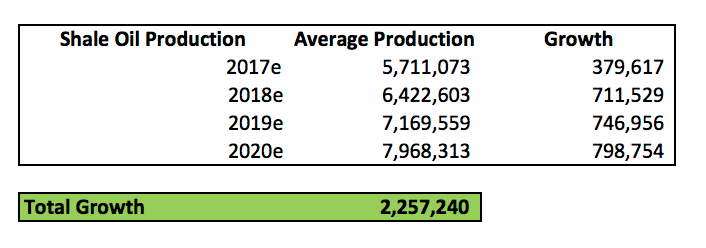

In our drilling productivity report on Monday, we wrote that U.S. shale - barring disappointing results out of the Permian - could still see growth of 711.529k b/d in 2018. Our estimate stems from taking peak well completion rates we've seen so far in 2017 and extrapolating them into 2018. We have now also revised higher ex-Permian shale production growth.

In total, this is what we see:

Now, OPEC with its vast amount of resources is probably getting the same results we got. Mark Papa, former CEO of EOG, noted in a presentation that U.S. shale will grow by only 600k to 750k b/d in 2018. Our estimate falls somewhere between that range.

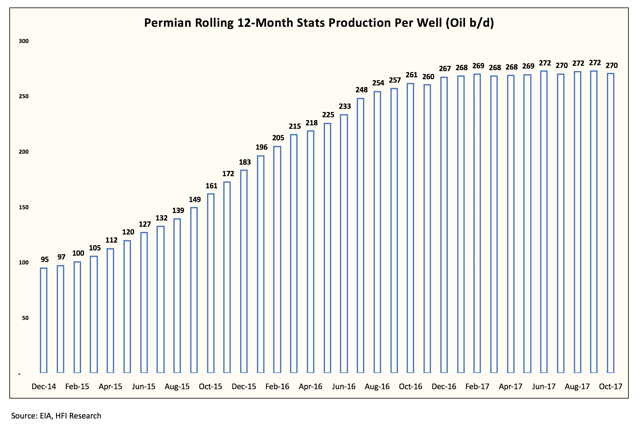

The reasoning for capped U.S. shale growth is quite easy to understand. First, U.S. shale productivity has stalled as expressed in production per well. As you will see below, Permian production per well has now been flat for over a year despite operator claims of better drilling results. Perhaps it's true on an individual basis, but we are not seeing this on a basin-wide basis.

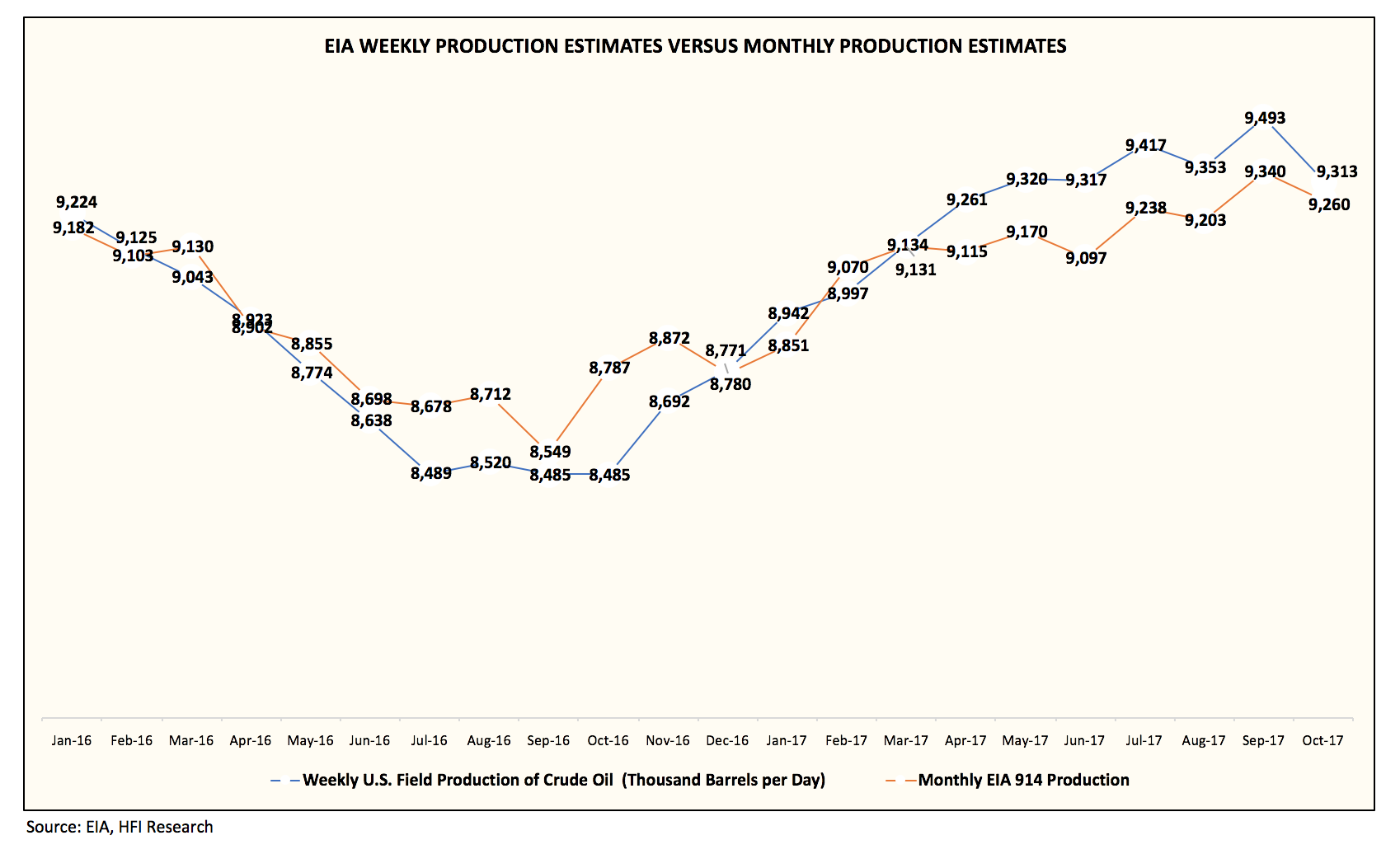

The second most obvious reason is that if U.S. shale had the capacity to increase production this year, we should have already seen it. But completion bottleneck continues to plague and drag production forecasts later than expected. In turn, we have this situation on our hands where EIA has massively overstated U.S. oil production in its weekly estimates.

From the onset, when the sell side started giving estimates of 1.2 to 1.4 million b/d, we knew those figures were off. In 2014, when rig counts were over a thousand and well completions were double the levels of today, U.S. shale grew at 1.2 million b/d. Yes, productivity has increased as you can see in that Permian production per well chart, but not to the extent that a single basin that produces 2.5 million b/d will grow at 50% year over year.

This leads us to our point of puzzle piece No. 3 - it doesn't matter if OPEC announces it this month for an extension to the end of 2018, because U.S. shale growth next year will be capped at around ~700k b/d. Announcing it now or announcing it in 2018 won't make a difference to this scenario.

Recap of the first three puzzle pieces

Puzzle piece No. 1 explains why Saudi didn't cut oil production, because it makes these decisions based on long-term fundamentals.

Puzzle piece No. 2 explains the long-term fundamentals and why a supply deficit is coming. This gives a tailwind for Saudi and OPEC to maintain the production cut.

Puzzle piece No. 3 explains that it doesn't matter if OPEC announces in November or Q1 2018, as U.S. shale production is capped next year.

Now we will explain the incentives of why announcing a deal extension in November benefits OPEC more than anyone else.

Puzzle Piece No. 4: Backwardation and how it hurts U.S. shale more than anyone else.

During the last three years, oil prices were in contango. This means that future oil prices were higher than prices today. This incentivizes traders to store crude to sell later at a higher fixed price (they can short the future price to hedge). This incentivizes producers like U.S. shale to hedge and receive a higher price with more certainty.

In all, contango oil price structure is exactly what saved U.S. shale companies from going bankrupt. They were able to hedge at higher prices and sell into more certainty. But the most important element that everyone seems to forget when it comes to analyzing U.S. shale is that servicing cost is based on promptoil prices and activities, not forward prices.

This insight has been discussed by some analysts before, but largely kept in the background. We know servicing cost inflation in drilling and equipment is rising, but how are they correlated? Service providers typically have some benchmark as to when they should start charging higher prices. It's never a fixed cost calculation, of course. If the producers are earning 20% more, my services should be 15% higher as one provider would reason. In addition, higher drilling and completion activities following higher oil prices manifest on themselves.

But what happens if the oil price curve is in backwardation? Let's say OPEC announces the production cut agreement will be extended to the end of 2018 on Nov. 30 -- the oil curve moves into massive backwardation with prompt WTI reaching $63, but the 2018 oil curve only averaging $56/bbl. For service providers, they can now start to reason with E&Ps that they should charge higher rates. "Look, oil prices are higher, and we agreed you would pay us higher X as oil increased."

In turn, what happens is if U.S. shale decides to start hedging after oil prices rise following the OPEC announcement, it will start seeing margins compress because servicing costs are based on prompt prices, not forward prices. This particular insight is interesting to us because it further enhances the incentives for OPEC to announce an extension to the end of 2018 in November.

Now, if we look at how OPEC gets its prices, the members get paid on prompt prices not forward prices. Thus, one can reason that backwardation is highly favorable for OPEC because cargoes are sold on the market rather than through hedges. In addition, if oil curve is in backwardation, it illustrates a tight physical market today and buyers willing to pay higher prices today than tomorrow. This then allows Saudi Arabia (for example) to increase its official selling price (OSP) to customers because barrels today are worth more than barrels tomorrow. This is when you start seeing Saudi raise OSPs on customers in Asia for example.

To sum up this puzzle piece, an announcement in November is highly favorable for OPEC. Servicing cost inflation squeeze resulting from a backwardated oil curve will push shale producer margins lower and force them to spend less on capex for production growth, while a backwardated oil curve is highly beneficial for OPEC.

Puzzle Piece No. 5: Saudi Aramco IPO and the importance of sentiment.

This puzzle piece gives us more certainty that OPEC will announce a production extension at the end of 2018 rather than the specific timing aspect. However, the economic incentives are aligned for Saudi to boost investor sentiment in the energy sector. It's no help when countries like Norway announce that it's planning to sell down the rest of its oil and gas exposure in its sovereign wealth fund, so sentiment for the Saudis becomes one of the most important factors to take into consideration.

When consultants and investment bankers are meeting with the Saudis, they will present what market multiples some of the oil majors are trading at. On an allocation basis, the chart below does not help Saudi's cause at all.

With investors obsessing over the threat of electric vehicles and renewable energy, Saudi has every incentive to make sure other energy companies benefit via more positive investor sentiment. As we have written repeatedly in the past, higher oil prices will rise all boats. Multiples will start to expand as investors pile back into energy stocks and, in turn, the multiple of Saudi Aramco when it does get sold for 5% to China or the public.

What about Russia?

You probably already read the article from the Financial Times saying that the Russians are questioning whether or not to extend the production cut to the end of 2018, or if it's wise to announce it so soon. The real reason why we don't even include Russia in our puzzle piece analysis is because President Putin has already come out strongly supporting an extension. Whatever headline you read over the next several weeks won't change any of this.

The main reason from our analysis is that President Putin's position in the Middle East now rivals that of the U.S. The strong relationship between Russia and Saudi Arabia further demonstrates what happens when the two largest oil producers come together to boost prices higher.

For Putin, the 2018 Russian presidential election on March 18, 2018, will be important. Why would you jeopardize the stability of the current economic environment over 300k b/d of oil? In addition, Russia has survived the last three years of oil price torment, and its economy is now geared to benefit from any upside in oil prices. This is also seen in its positive year-over-year GDP growth of 1.08%. If keeping its producers in check for an extended nine months could see oil prices well supported, what's the reason not to support this deal?

Putting it all together: How are we so sure that OPEC and non-OPEC countries will announce a deal extension to the end of 2018, let alone announce it at the end of November? In our view, the recent media coverage on OPEC gives readers pause as to whether or not there will even be an extension following Q1 2018.

But as our very first variant perception insight tells us, this production cut agreement isn't a real production agreement. The same reasoning that was used for why OPEC and non-OPEC countries would extend the production agreement in May 2017 to the end of 2017 and into Q1 2018 continues to apply for why there will be another extension to the end of 2018.

Our analysis points to the five puzzle pieces as the main points for why an extension will happen, and why it will happen on Nov. 30. A strongly backwardated oil curve will push servicing cost inflation higher and squeeze shale's ability to hedge into higher prices, while simultaneously benefiting OPEC's own selling price.

A supply deficit is coming in the long-term forecast, providing tailwinds for OPEC to increase production in 2019 if it so chooses. Shale's capped production growth in 2018 allowing OPEC to push the market into an even tighter supply situation, and, finally, there's the Saudi Aramco IPO providing the needed sentiment flip the Saudis so desperately need today.

The main concern in the market continues to be what happens to U.S. shale production if OPEC and non-OPEC countries announce a deal extension at the end of November. We hope that our article and previous ones explain why a material rise in U.S. shale production is not possible given the current servicing constraints. In addition, a strongly backwardated oil curve and lack of external financing raised in 2017 could further dampen shale's ability to grow.

In summary, we see the incentives aligned for OPEC and non-OPEC to announce a deal extension at the end of 2018 in November.

Supplemental Reading

- Last Year's Macro Edge Was Understanding OPEC, This Year, It's Understanding U.S. Shale

- Shattering The Complacent View, U.S. Shale Oil And Natural Gas Production Growth Forecasts Are Nowhere Near As Optimistic As People Think

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.