.jpg)

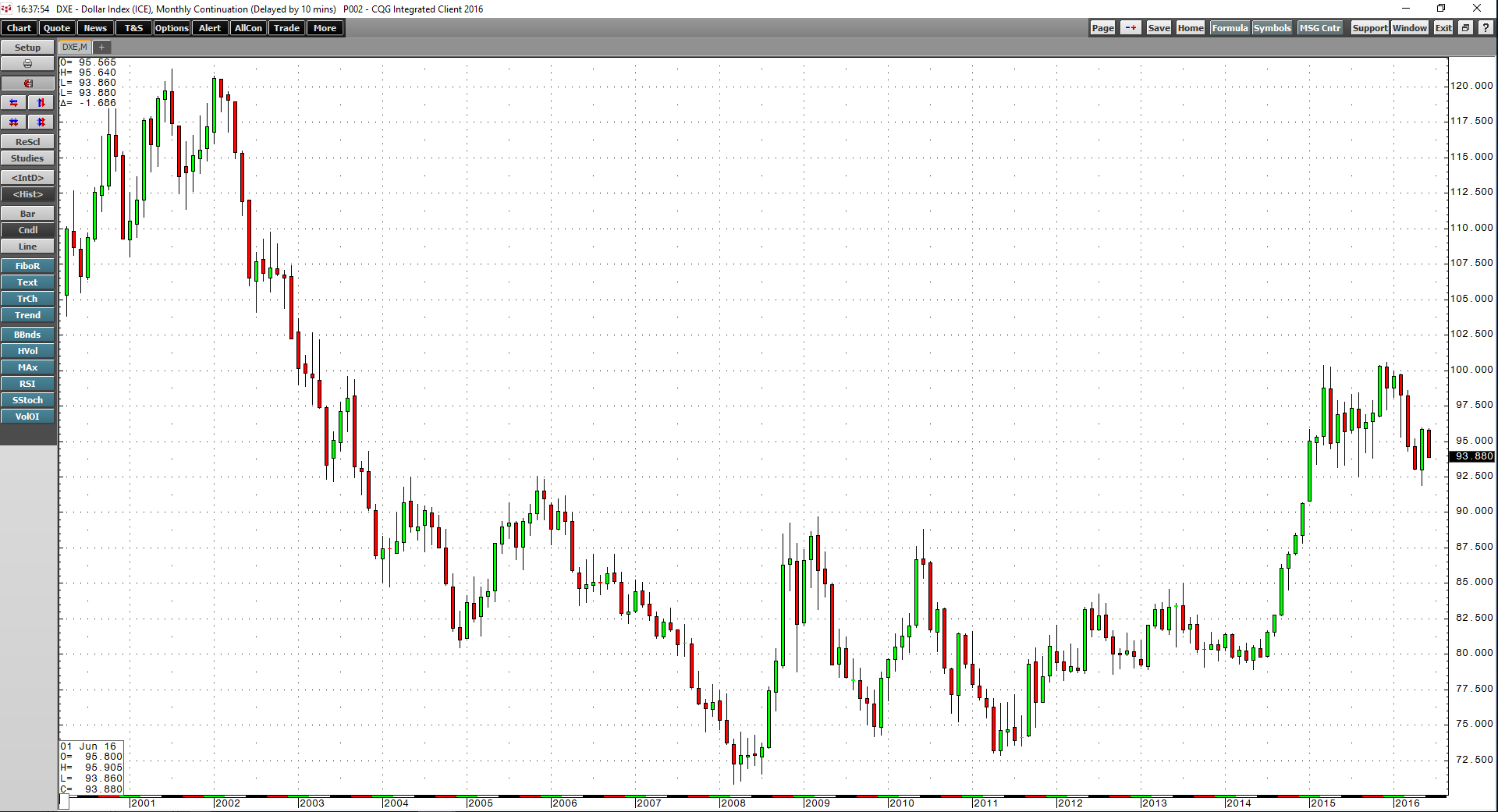

Commodity markets are cyclical in nature. Each raw material market has its individual characteristics. So many factors contribute to whether the price of a commodity moves higher or lower. While commodity production is often a localized affair, consumption is ubiquitous. Therefore, deficit conditions or periods of oversupply occur often as a result of weather or other acts of nature, political events, and a myriad of other factors. However, commodities are also an asset class that responds to macroeconomic forces. In 2004, the raw material markets embarked on a bull run that took the prices of many raw materials to all-time highs. Before 2004 crude oil had never traded above $42 per barrel and in 2008, the price peaked at over $147. Gold had never traded above $875 per ounce before 2008 and in 2011 it peaked at over $1900. Copper, sold for over $4.60 per pound that year, before 2005 the price never exceeded $1.61. It was not a one-way ride for commodities which are some of the most volatile assets that trade on futures exchanges. In fact, the global economic crisis of 2008 caused prices to plunge, but they recovered quickly due to central bank policies of low interest rates and quantitative easing.

There are many reasons that commodity prices took off and moved to dizzying heights as an asset class. Low interest rates and a weak dollar were both contributing factors. However, in 2011/2012 many commodities began to fall as gravity hit the asset class like stones falling from a cliff. High prices had caused an increase in output and a global economic slowdown caused inventories to rise and demand to fall. Raw material prices had already been falling when the dollar began to move higher in May 2014, and a strong dollar hit the sector like a ton of bricks, turbo-charging the descent of many prices across the asset class. By late 2015 and early 2016, many commodities had halved in price or worse. Crude oil fell to lows of $26.05 per barrel on February 11, 2016. Copper hit lows of under $1.94 per pound in January. In December 2015, gold fell to $1046 per ounce and silver which peaked at over $49 per ounce in 2011 dropped to below $13.70. The almost eight-year bull run in commodities had turned into a four-year bear.

The bear turns bull

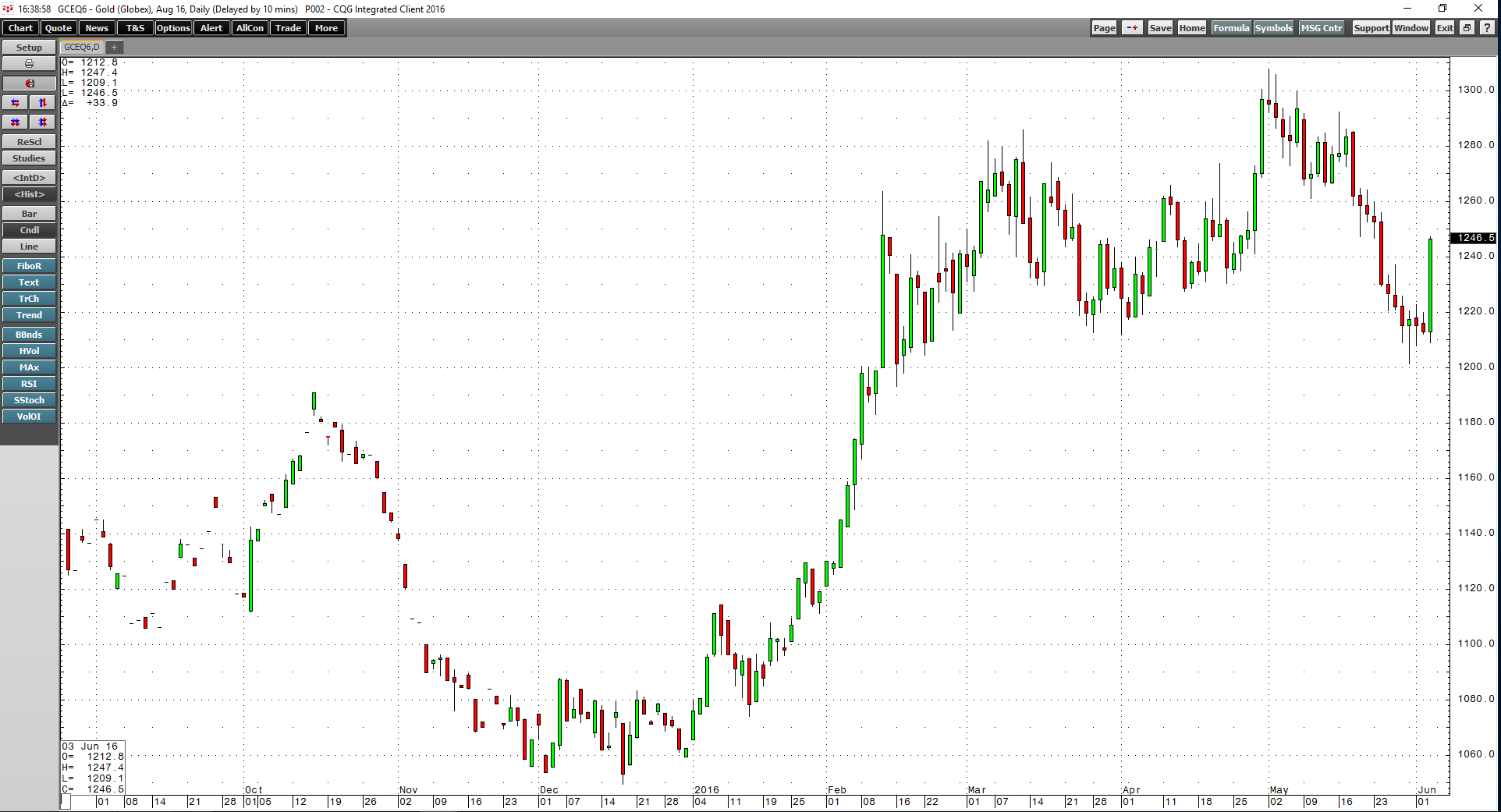

A fast and furious recovery in many commodity prices occurred over recent months. Gold rose from $1046 in late 2015 to $1306 at the beginning of May - an increase of 24.9%. Silver rose from $13.635 in December 2015 to $18.06 on May 2, 2016, it appreciated by 32.5%. The price of soybeans has rallied over recent weeks along with many other agricultural commodities. Sugar, which was trading at 10.13 cents per pound, last August, reached highs of 18.79 just last week, an increase of almost 86% from the lows. Most dramatically, crude oil futures have exploded from $26.05 on February 11 to $50.21 per barrel on May 26. The price of crude oil had increased by 92.7% in less than four months.

Recently, the dollar has appreciated, and the U.S. Federal Reserve has reiterated their intentions to hike interest rates this summer and many commodities have either moved lower or stopped their upward trajectory. The dollar is the reserve currency of the world and the pricing mechanism for most raw materials around the world. A stronger dollar is not supportive of a continuation of the recovery in commodity prices.  In May, the dollar put in a bearish key-reversal trading pattern on the monthly chart and one of the first commodities to recover in 2016 has also hit the skids as the gold price has moved significantly lower since making highs at the beginning of May, until last Friday.

In May, the dollar put in a bearish key-reversal trading pattern on the monthly chart and one of the first commodities to recover in 2016 has also hit the skids as the gold price has moved significantly lower since making highs at the beginning of May, until last Friday.  Gold traded to lows of just over $1200 per ounce last week, over $100 below the May 2 highs. Many were asking if the bear that turned bull was becoming a bear again and if the commodity rally of 2016 was nothing more than a bear market correction. The bullish key-reversal trading pattern on the daily chart probably will end those questions for the near future.

Gold traded to lows of just over $1200 per ounce last week, over $100 below the May 2 highs. Many were asking if the bear that turned bull was becoming a bear again and if the commodity rally of 2016 was nothing more than a bear market correction. The bullish key-reversal trading pattern on the daily chart probably will end those questions for the near future.

There are four important reasons why I believe that the commodity bull remains strong. I think that commodities have turned the corner and while they may not go up in a straight line, higher lows, and higher highs are in store for the sector for the coming months.

Reason one- Markets overshoot

Commodities are volatile assets. It is not unusual for the price of a raw material to double, triple, half or more over a very short period. The bear market that took prices lower until recently suffered from the same mania that took prices to ridiculous highs in 2011/2012.

Commodities as an asset class transformed from alternative instruments only available to the few brave enough to enter the shark-infested waters of futures and futures options markets to the mainstream starting in 2004. The advent of ETF and ETN products that replicated price action in the physical and futures markets brought commodities trading, speculation and investing to equity portfolios all over the world. Market participants no longer had to worry about margin calls in the futures markets. Now there are market vehicles that move up and down with commodity prices. If raw material variance is too tame for some, financial engineers developed leveraged ETF and ETN products that would satisfy the market's lust for action by providing double and triple returns on the up and down moves in these volatile assets. These products caused a herd of buying on the way up, and herds of selling on the way down in commodity markets as new capital came to the markets exacerbating market moves and highs and lows.

Commodities always have overshot highs and lows due to speculative behavior. As an example in 2011, the price of cotton rose to $2.27 per pound putting many in the industry out of business. They went short cotton at prices never seen before and were carried away to bankruptcy as margin calls swallowed their capital. Cotton never traded above $1.172 per pound until it moved to almost double that level in 2011. Today, cotton trades at less than 65 cents per pound.

I believe that while commodities have always been and will always be volatile and wild markets, ETF and ETN products have added to that volatility causing them to overshoot on the upside and the downside. The highs of 2011 and 2012 were an extension, and the lows we saw in 2015 and early 2016 were another extension.

Commodity prices went too high in 2011/2012, but they also fell too hard to levels that are unsustainable in late 2015 and early 2016.

Reason two- Global interest rates remain low

Commodity prices are highly sensitive to interest rates around the world. When interest rates are high, it costs more to carry inventories of raw materials. Therefore, consumers tend to become hand to mouth regarding their requirements. Low interest rates are positive for commodities, and we continue to live in an environment of some of the lowest interest rates ever on record.

There is much ado about the Fed's intention to jack up interest rates this summer, but let's remember which levels they are rising from and to. Even after a dramatic increase by the Fed, rates will still be below 1%, a level that is unprecedented until the financial crisis of 2008 and the quantitative easing tools used by the central bank. Interest rates remain in negative territory in Japan and Europe - it costs money to store money in the bank. No economic text accurately explains and deciphers this condition today; it never existed before.

The fact is that the global economy continues to be weak, and central banks continue on the path of stimulating economies with low rates. Encouraging spending and borrowing at the expense of saving is a path that leads to more paper money floating around the globe that has less and less value as time goes on. The ultimate price for the global central bank policy of low interest rates is likely to be inflation. Unprecedented low rates could lead to record levels of inflation. In an inflationary environment, the purchasing power of money declines. Inflation is a commodity's best friend.

Reason three- The economics of commodities

Commodity prices rose to levels in 2011/2012 where producers profited beyond their wildest dreams. At those prices, they increased output to capture even more profits as the bull market seemed like it would never end. Fear and greed always drive markets and for commodity producers, the period leading up to the highs five years ago made their mouths water and their pockets fill with cash.

When Glencore, the largest independent commodity trader in the world went public, many of the higher-level traders became billionaires. When the company decided to purchase Xstrata, a commodity producer, the debt they took on was a pittance compared to what they believed they would pocket if the raw material bull market kept charging higher. However, that debt became a stranglehold around their necks as prices dropped and they could not service the massive debt load on their balance sheet. Glencore has wisely been selling off assets to pay down debt to survive.

Glencore is a case study when it comes to all producers who thought the good times would continue. Prices rose to a level where demand fell, and inventories started to grow in a vicious cycle that defined the period from 2011 through early 2016. Now, output has slowed to a point where stockpiles will begin to diminish. At the same time, prices have dropped to levels where consumer demand will increase if for no reason other than more people on the planet will require and consume more commodities. It may take some time for inventories to fall, but they will, and once raw material markets move into deficit, prices will rise again.

The perfect example is the sugar market which is now entering its second year of deficit conditions. The price of sugar has moved from just over 10 cents per pound to almost 19 cents in less than one year. We are seeing a similar reaction in natural gas in the U.S. over the past week. In March the price of the energy commodity fell to the lowest price since 1998 when it traded at $1.6110 per MMBtu in early March. The price dropped so low that producers have decreased output. Injections into inventory this spring have been far less than last year and the price has begun to rise trading above the $2.40 per MMBtu level last Friday.

Classic economic theory says little about negative interest rates, but it does teach that prices tend to increase to a level where demand falls and inventories rise. When prices fall, and stockpiles decline, demand tends to grow causing prices to rise once again. This proven theory of price action is the basis for the cyclical nature of commodities. I believe that while it may be a bumpy road, commodity prices reached a critical nadir as an asset class in late 2015 and early 2016.

Reason four- Explosive population growth versus finite raw materials

The fact is that the addressable market for commodities consumption has risen dramatically over recent years for two reasons. Population continues to grow exponentially. In 1959, when my mother hatched me, there were 2.9 billion people on planet earth. Today more than 7.3 billion humans occupy the globe. Secondly, and perhaps more compelling, standards of living around the world have also increased. As people become accustomed to a better life, human nature drives them to want more stuff. They become bigger consumers of commodities. A bowl of rice is not what it used to be for many, now a steak or grain-based protein is what they desire. And, throw in a cup of Starbucks and a chocolate bar for good measure in places like China and India.

Commodities are finite assets; the population is not. The demand side of the commodity equation continues to increase on a daily basis. Once raw material inventories fall, it will be off to the races again for the prices of staple goods. Raw materials will naturally make higher lows and higher highs in the years to come; it is a simple case of rising demand.

For those reasons and more, I believe that commodity prices will not return to levels seen earlier this year and late last year. Crude oil below $30 per barrel was an aberration. Sugar at 10 cents per pound is not in the cards. Buying on dips and taking profits on rallies could be the best way to optimize in the commodity markets in the months ahead. The demand side of the equation continues to stretch the fundamentals and lead to a bumpy ride of higher lows and higher highs in the future. That is the reason that commodities will continue on their wild ride making the raw material markets a trader's paradise and an investor's nightmare. Fasten those seat belts and enjoy the ride.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.