.jpg)

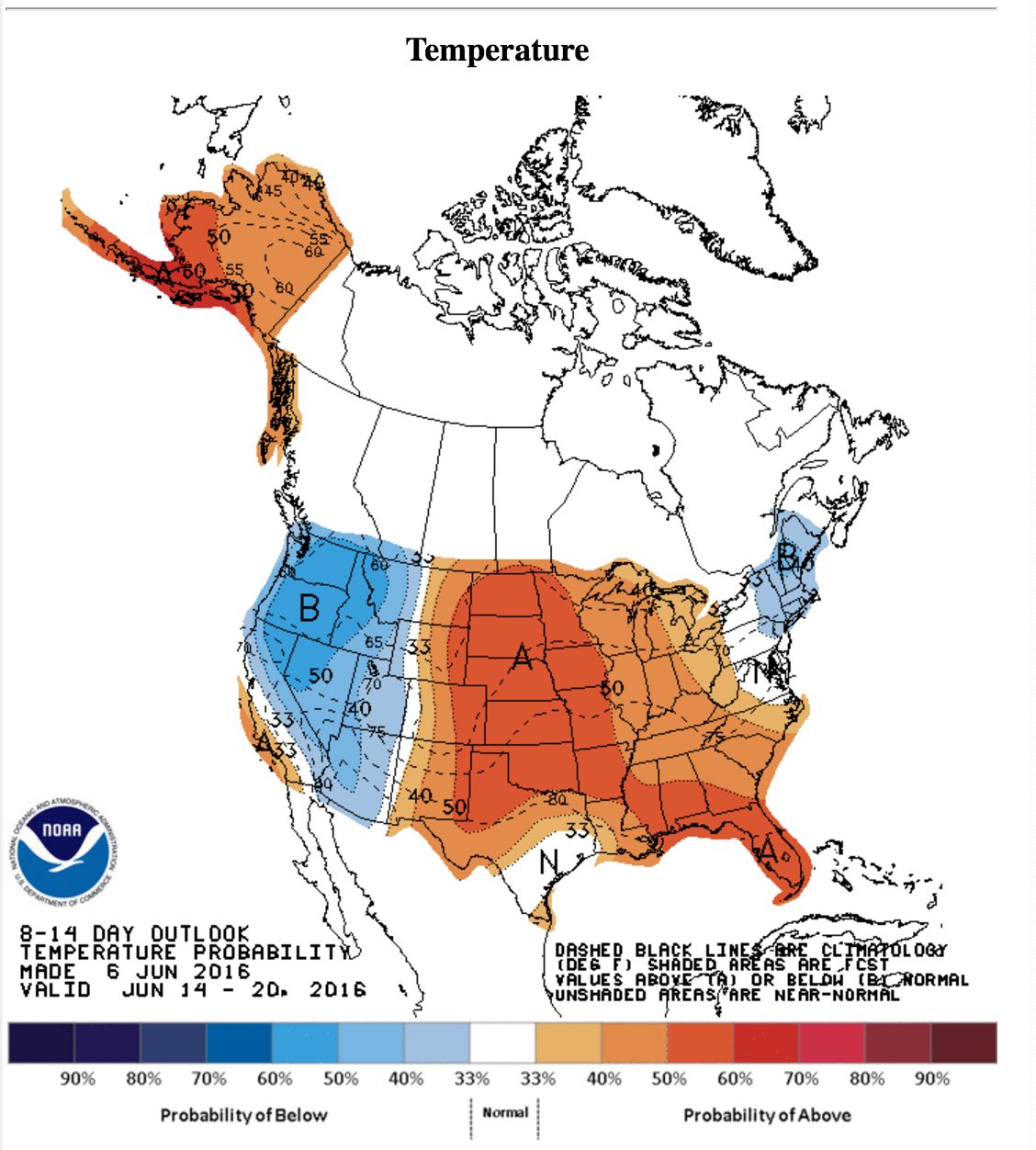

Prices continued to rocket higher today despite a slightly more bearish weather forecast in the 8-14-day outlook.

Despite the recent price increase, natural gas prices remain below the "pivotal" $2.50/MMBtu mark. Traders we've spoken to say this will prove to be a strong resistance for prices. Surplus storage will need to continue to shrink and US gas production needs to continue to decline. To put it simply, fundamentals need to catch up to the recent price move upwards.

RBN Energy came out today revising their end of injection estimate once again. The reason continues to be attributed to more "bullish" physical flow. With US gas production in decline, one has to start wondering what happens to prices when all of the surplus goes away?

For most natural gas producers, the idea of having prices above $4/MMBtu is similar to saying oil prices will be above $100. Even though the price was there just a few years ago, producers have gone through so much pain that the moment prices increase, hedges will fly in. This will somewhat insulate producers from producing all out, but it will incentivize additional production to come online. So far this year, most producers we follow have either allowed production to decline or drill DUCs to keep production flat. Out of all of the producers we follow, there are a handful that are increasing natural gas production while everyone else continues to struggle. The producers that are increasing production are doing so via debt and equity financing, and no one is able to grow within cash flow this year.

If supply won't rebound fast enough in response to prices, what will happen?

Surplus storage will likely keep a lid on prices, and if prices increase too fast, wells that have been shut-in due to uneconomic prices will likely be brought back on. Canadian gas storage remains bloated, and Canadian gas imports will likely rise dramatically to 6.5 Bcf/d + to bring in the needed gas. But with Canadian storage only around 592 Bcf, the 1.5 Bcf/d increase in exports will likely draw down excess storage within eight weeks in the winter months.

Prices in response will likely rise to $4/MMBtu-plus in the short run allowing producers to hedge in prices. This will likely result in additional supplies coming online in 3-6 months and bringing gas storage back to the five-year average. Obviously, anything after that will be subjected to the weather, and we have no idea what weather looks like next year.

We continue to be bullish natural gas (NYSEARCA:UNG) prices, and in turn we have positioned ourselves accordingly in the names that we believe have not priced in a commodity price recovery. The HFI portfolio since launch has outperformed the S&P 500 by 14.07% and returned 24.86% on a gross basis.

For investors interested in how we are managing the portfolio, please considersigning up for our premium service. We look forward to you joining the HFI community. And as always, if you liked our natural gas daily write-up, please be sure to click follow and read our other articles as well!

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.