.jpg)

The market continues to exhibit large negative divergences. This characteristic has historically occurred at times preceding rough periods in the stock market. For instance, the summer of 1987 was plagued by narrow breadth, directly followed by a crash that fall. In the summer of 1998, there were clear warning signs leading into the Thai baht crisis, which triggered an international crash of stocks. A similar situation occurred at the start of 2008, directly before the mortgage crisis. Prudent investors would be foolish to ignore the current warning signs.

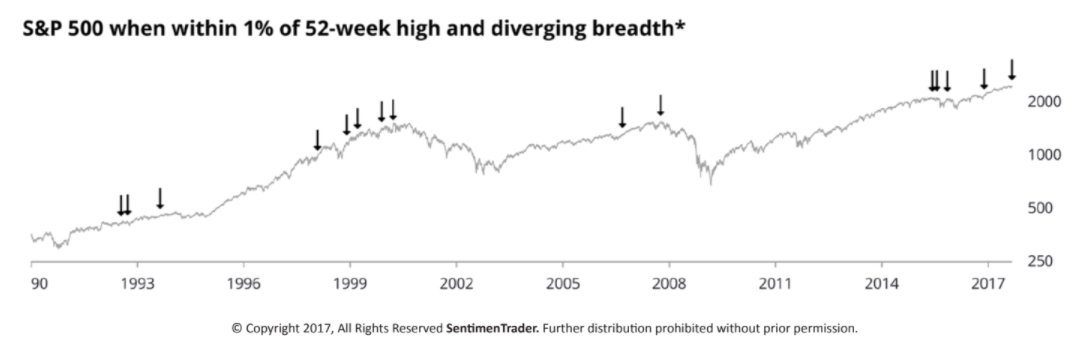

The cumulative 21-day advancing/declining volume indicator measures the internal dynamics of the market by monitoring up/down volume. We have highlighted the previous four peaks in order to emphasize the series of lower highs in the up/down volume gauge. This situation has occurred while the indexes have simultaneously hit higher highs - a classic negative divergence, illustrating that large institutional sponsorship has not been following the indexes.

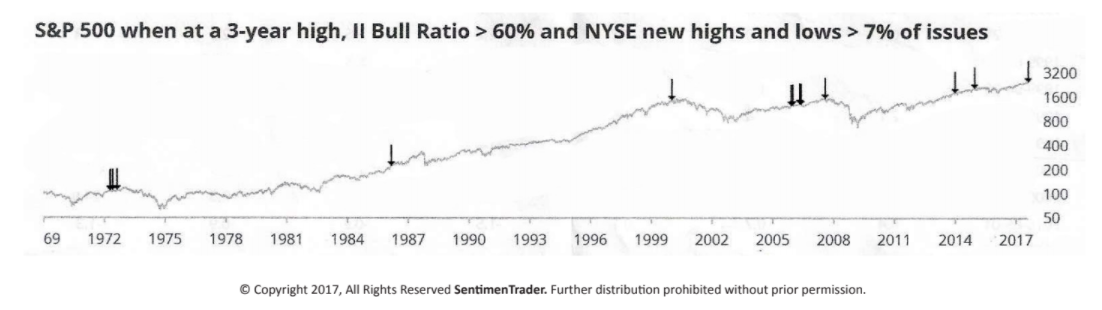

Well-known quant Dr. John Hussman says we are experiencing one of the most dangerous markets in history. He bases his assessment on three simultaneous criteria. Hussman warns of risk when the S&P 500 is at a three-year high, the investors-intelligence bulls/bears exceed 60% and the NYSE new highs and lows are greater than 7% of issues. This chart identifies such occurrences. Note that in 2000, and then again in 2007-08, substantial corrections followed warning signals. It is notable that the signal was just shy of being triggered a week prior to the 1987 crash. Over the past nine quarters, three sell signals have been triggered.

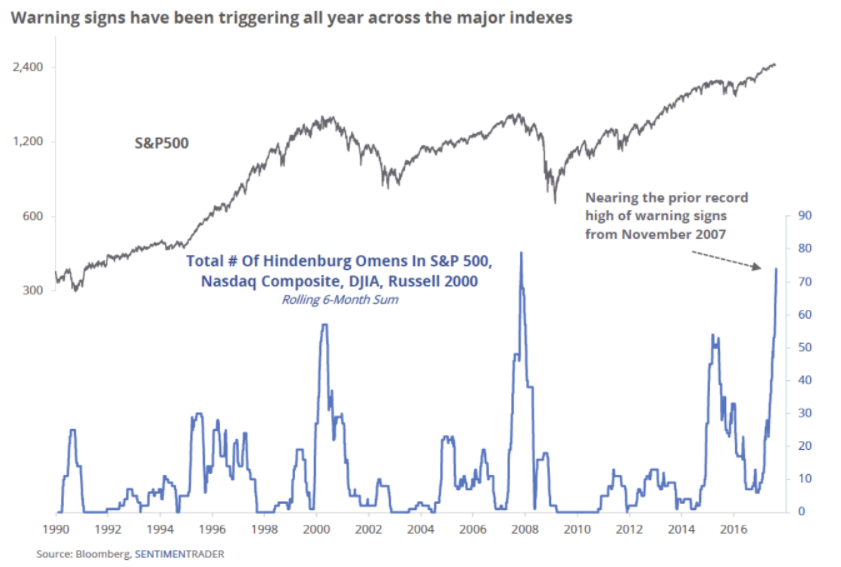

Named after the crash of the German airship in the late 1930s, the Hindenburg Omen is a technical indicator developed to predict the potential for a financial market crash. In August, Hindenburg omens occurred five times during a six-day period. A Hindenburg Omen is created when:

• The S&P 500's five-day moving average is higher than it was the day before

• The McClellan Oscillator is below zero

• The 52-week highs are greater than 2.2%

• The 52-week lows are greater than 2.2%

Sentimentrader.com has created a study, going back to 1990, that tracks the occurrence of Hindenburg omens during a six-session period. Arrows on the chart indicate when each omen has been triggered. The S&P (NYSEARCA:SPY) (NYSEARCA:SH)has not suffered five signals so tightly clustered since 2007, and prior to that 2000. Poor performance after each omen can be tracked by viewing each red number on the table. This is yet another clear instance of statistical negative divergence.

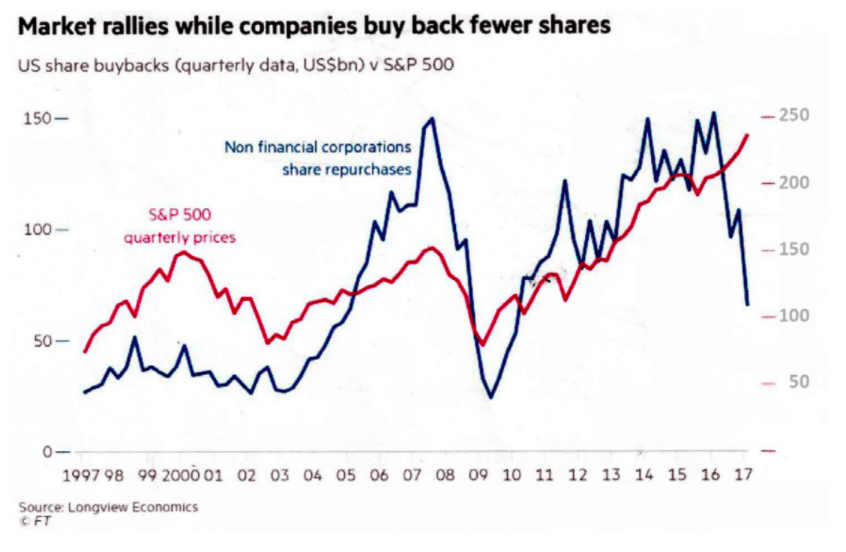

Corporations have been one of the largest buyers of their own shares throughout the recent bull market. Over the last year, however, share repurchases have dropped to a four-year low. This sharp drop takes away liquidity and highlights the fact that increasing numbers of publicly traded companies see little value in their own company stock.

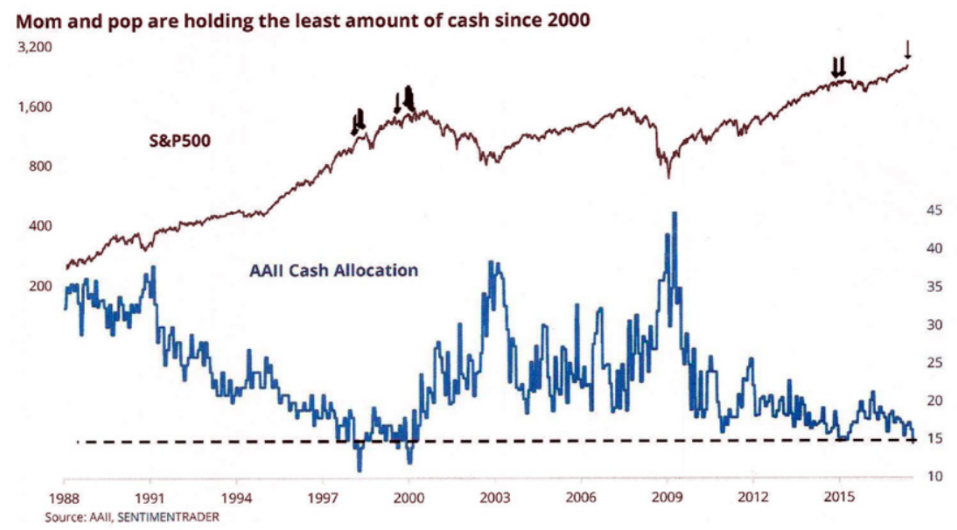

According to the latest poll by the American Association of Individual Investors, mom-and-pop investors have the lowest cash cushion since 2000, holding only 14.5% of their portfolios in cash. The chart highlights each date, going back to 1987, when investors' cash allocation fell below 15%. Retail investors are traditionally reactive participants. It is interesting to note their horrendous one-year returns following each signal. At the bottom in 2009, mom-and-pops held the most amount of cash. The sentiment is overly optimistic because they are now fully invested.

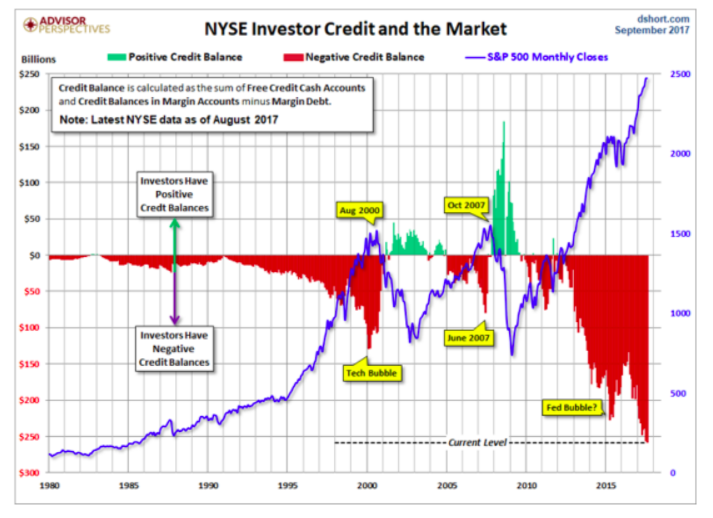

The NYSE recently released a worrisome investor credit report, which discloses the sum of the free credit cash accounts and credit balances in margin accounts minus margin debt. The current debt dwarfs the 2000 and 2007 periods, which both preceded bear markets. The most significant issue with margin is that it creates extremely weak shareholders that can be pushed out of their positions due to margin calls. The current situation sets the stage for a tremendous number of margin calls in the next decline, which could exacerbate selling.

Conclusion

An escalating market, accompanied by lackluster participation and intensifying divergence, indicates trouble ahead for the stock market. With the NYSE debit balances reaching an all-time high, accompanied by weak corporate buybacks, one must wonder where future buyers will be found. The glass is full and is now overflowing. We remain 50% short.

Disclaimer

Lamensdorf Market Timing Report is a publication intended to give analytical research to the investment community. Lamensdorf Market Timing Report is not rendering investment advice based on investment portfolios and is not registered as an investment advisor in any jurisdiction. Information included in this report is derived from many sources believed to be reliable but no representation is made that it is accurate or complete, or that errors, if discovered, will be corrected. The authors of this report have not audited the financial statements of the companies discussed and do not represent that they are serving as independent public accountants with respect to them. They have not audited the statements and therefore do not express an opinion on them. The authors have also not conducted a thorough review of the financial statements as defined by standards established by the AICPA.

This report is not intended, and shall not constitute, and nothing herein should be construed as, an offer to sell or a solicitation of an offer to buy any securities referred to in this report, or a "buy" or "sell" recommendation. Rather, this research is intended to identify issues portfolio managers should be aware of for them to assess their own opinion of positive or negative potential.

The LMTR newsletter is NOT affiliated with any ETF's Nor any investment Advisors.